Users paid $9.7 billion in on-chain fees in the first half of 2025, up 41% year over year and the second-highest total on record.

1kx projects more than $32 billion in on-chain fees for 2026, driven by accelerating application growth. That growth has pushed the word “revenue” into every crypto investor pitch deck, every sector report, and every valuation conversation.

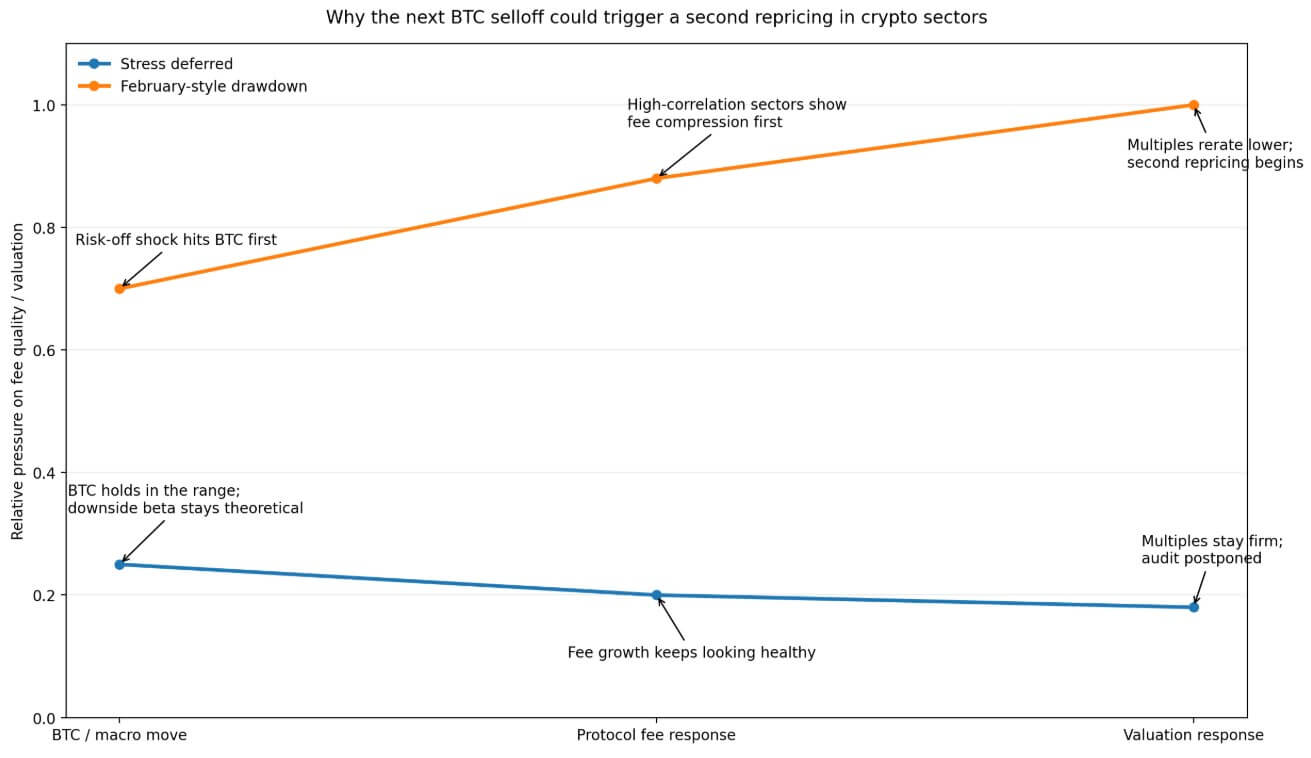

The report added that a Bitcoin drawdown may stress-test protocol fees.

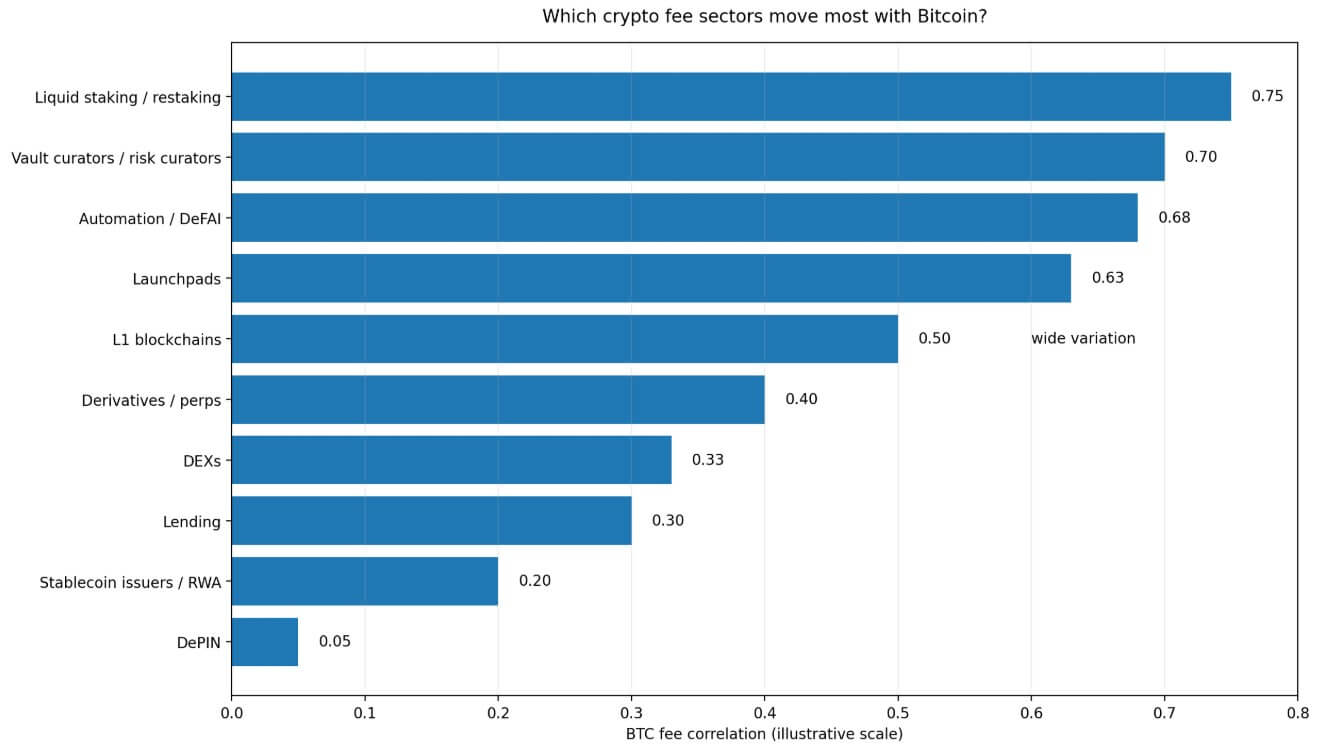

1kx’s April sector analysis finds that nearly every crypto fee category shows a positive correlation with BTC price. There is also wide dispersion across sectors, and the critical variable of downside beta is still unresolved.

The firm says a 0.6 correlation can mean very different things depending on whether sector fees fall at 0.8x Bitcoin’s pace or at 1.5x, and it identifies the decomposed upside versus downside fee sensitivity.

In crypto, a fee line can look like a business in an up market and still trade like amplified BTC beta when macro fear arrives.

The reflexive fee cluster

The sectors 1kx identifies as most correlated with Bitcoin price share a common economic architecture that improves when prices rise and deteriorates when they fall, often faster than the underlying asset itself.

Liquid staking and restaking sit at the top of that cluster, with their fee streams depending on yields that expand as borrowed capital and risk appetite grow and contract as they retreat.

Vault curators face the same pull, as assets flow in when price momentum is positive and out when sentiment reverses. Launchpads are the most acutely sentiment-driven category in the report, with launch activity accelerating in directional bull markets and stalling when confidence cracks.

Automation and DeFAI protocols, which earn fees tied to transaction activity and strategy deployment, also track the same directional pulse.

1kx says that layer-1 (L1) blockchains’ fee correlation to BTC varies widely, with many inheriting market direction through native token price movements and activity mix, while others show more independence depending on their application base.

That variability makes the directional pull of token prices on on-chain activity mean most L1s still carry meaningful BTC sensitivity in their fee lines.

Reflexivity connects these categories, as their fees are largely an output of the same speculative, position-driven activity that drives Bitcoin itself.

When investors talk about fee growth in these sectors during an up market, they are partly describing business momentum and partly describing the same macro tailwind that lifted every risk asset in the portfolio.

The delivered-services layer

DePIN stands apart in 1kx’s framework as the lowest-correlation category, earning the distinction as the standout for non-directional crypto revenue exposure.

The reason is that DePIN fees track the dollar value of compute, bandwidth, storage, and other delivered services. Demand for those services comes from users with real operational needs, and while token prices affect incentive structures, they do not directly set the fee rate, as asset prices do for yield or launch activity.

1kx projects DePIN fees above $450 million in 2026, sustaining triple-digit growth.

Stablecoin issuers and real-world asset protocols sit in a similar lower-correlation band, with 1kx estimating their BTC correlation at roughly 0.2. Their fee economics depend more on issuance volume, reserve management, and AUM than on speculative trading alone.

A lower correlation indicates a fee structure less tied to BTC price direction. 1kx’s framework supports “more differentiated revenue exposure” and stops well short of claiming immunity to a selloff.

The more precise claim is that DePIN and issuance-linked businesses have a better structural case for defending their fee lines during a BTC-specific drawdown.

| Sector group | Main fee driver | Behavior in an up market | Likely stress in a drawdown | Article takeaway |

|---|---|---|---|---|

| Liquid staking / restaking | Yield, leverage, risk appetite | Fees expand quickly | Yields compress, activity fades | Most reflexive |

| Vault curators | AUM, momentum, inflows | AUM rises with price | Outflows can hit faster than BTC | High downside sensitivity risk |

| Launchpads | Sentiment, launch activity | Strong in bull phases | Launch volume can stall fast | Highly cyclical |

| Automation / DeFAI | Strategy deployment, transaction activity | Benefits from active markets | Usage may fall with risk appetite | Directional fee exposure |

| DePIN | Compute, bandwidth, storage demand | Growth tied to service usage | More insulated from BTC-specific shocks | Most differentiated |

| Stablecoin / RWA | Issuance, reserves, AUM | More gradual growth | Less directly tied to BTC moves | Lower-correlation fee exposure |

| DEX / Lending / Perps | Volume, rates, volatility, leverage | Can benefit from activity | Mixed; volatility helps, unwinds hurt | Contested middle ground |

Decentralized exchanges (DEXs), lending protocols, and perpetuals platforms occupy a contested middle ground. 1kx puts DEX median correlation at roughly 0.33 and lending at around 0.3, while derivatives show wide variation, sometimes exceeding 0.4.

Volatility can support trading volume even in down markets, providing these sectors with a partial buffer. Still, fee-rate compression and position unwinds during stress episodes make their revenue lines unstable in ways that simple average correlation fails to capture.

Why valuation is the real payoff

1kx’s broader revenue report shows that price-to-fee ratios across crypto sectors span several orders of magnitude. Blockchains had a median P/F ratio of 3,902x in the third quarter of 2025, with L1s at around 7,300x, compared with 17x for DeFi and finance.

DePIN’s median P/F ratio had fallen to 211x from roughly 1,000x a year earlier. Blockchain valuations still account for more than 90% of the analyzed fee-generating market cap, even though DeFi and finance produce most of the fees.

1kx also says fee changes lead valuations in DeFi and finance, and to a lesser extent in blockchains.

If that directional relationship holds on the downside, with fees dropping first and multiples compressing in the weeks that follow the initial price move, then a BTC drawdown that exposes fee fragility in high-correlation sectors could trigger a second-order valuation adjustment.

Investors who had assigned business-quality valuations to beta-exposed fee streams would face a rapid repricing.

The test gets deferred

If macro conditions keep easing, such as oil lower, Fed-cut expectations holding, and geopolitical risk fading, Bitcoin could keep holding firm in the mid-to-high $70,000s and push toward Citi’s 12-month base target of $112,000.

In that environment, fee lines across most sectors would continue to expand, and the downside beta would remain theoretical. 1kx projects application-led fee growth accelerating into 2026, with DeFi and finance expanding above 50% year over year.

The risk in that scenario is that the market continues to treat cyclically strong fee growth as evidence of durable business quality. Launchpad activity stays elevated in a buoyant market, restaking yields look robust when risk appetite is healthy, and vault curators report strong AUM figures.

The audit gets postponed, and capital keeps flowing into sectors whose fee quality has never been tested under real stress. The environment of falling oil, easing inflation fears, and revived Fed-cut bets is exactly the kind of environment where that postponement extends.

February repeats at scale

On Feb. 5, Bitcoin fell 14.1% to an intraday low of $62,254.50 in a single session as risk sentiment weakened, tech stocks sold off, and ETF outflows accelerated.

The crypto market shed roughly $2 trillion from its October peak during that episode. Launchpad activity cooled, borrowed-capital positions unwound, and restaking yields compressed.

Fee lines that had looked impressive through the end of 2025 showed their directional dependence within a matter of weeks.

A repeat of that pattern would move the downside-beta question from 1kx’s stated next step to a live market event.

Sectors with reflexive fee structures would face the hardest examination, with the market looking for launchpads seeing launch volume decline, restaking yields compressing as borrowed capital exits, and vault curators watching AUM decline faster than token prices.

DePIN and issuance-linked businesses would still face headwinds, but their relative fee resilience would become legible in the data for the first time.

If fee changes drive valuations in DeFi and finance higher, the same mechanism works in reverse.

Protocols that report fee compression in the first quarter of the next down cycle give the market a reason to compress their multiples before the full macro picture has even resolved.

Investors who had assigned business-quality valuations to beta-exposed fee streams would face a rapid repricing.

Bitcoin is currently around $78,000, holding near the top of its recent range from the April geopolitical relief rally, exactly the window in which the fee-quality question sits unresolved.

The post Crypto traders spend $9.7B on fees as the next Bitcoin drawdown will expose which on-chain costs are real appeared first on CryptoCho

{kind=link}